Broadcom Stock: Is Wall Street Bullish or Bearish?

/Broadcom%20Inc%20logo%20on%20building-by%20Poetra_%20RH%20via%20Shutterstock.jpg)

Broadcom Inc. (AVGO), headquartered in Palo Alto, California, is a global technology leader that designs, develops, and supplies various semiconductor devices, with a focus on complex digital and mixed-signal complementary metal-oxide-semiconductor-based devices and analog III-V-based products. With a market cap of $1.4 trillion, the company offers storage adapters, controllers, networking processors, motion control encoders, and optical sensors, as well as infrastructure and security software to modernize, optimize, and secure the most complex hybrid environments.

Shares of this semiconductor giant have significantly outperformed the broader market over the past year. AVGO has gained 105% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 19.3%. In 2025, AVGO stock is up 31.1%, surpassing the SPX’s 8.4% rise on a YTD basis.

Zooming in further, AVGO’s outperformance is also apparent compared to the SPDR S&P Semiconductor ETF (XSD). The exchange-traded fund has gained 25.7% over the past year. Moreover, AVGO’s double-digit gains on a YTD basis outshine the ETF’s 8.4% returns over the same time frame.

AVGO’s strong growth can be attributed to its booming artificial intelligence semiconductor business, with custom AI accelerators and AI networking showing significant growth. The company's robust networking portfolio is supporting the development of AI systems in large cloud data centers. Additionally, the integration of VMware has driven solid results in infrastructure software, with a shift to subscription-based models driving steady gains. With strong demand in both AI hardware and software, Broadcom's outlook remains positive.

On Jun. 5, AVGO reported its Q2 results, and its shares closed down by 5% in the following trading session. Its adjusted EPS of $1.58 beat Wall Street's expectations of $1.57. The company’s revenue was $15 billion, surpassing Wall Street forecasts of $14.95 billion. For Q3, AVGO expects revenue to be $15.8 billion.

For the current fiscal year, ending in October, analysts expect AVGO’s EPS to grow 47.7% to $5.48 on a diluted basis. The company’s earnings surprise history is mixed. It beat the consensus estimate in three of the last four quarters while missing the forecast on another occasion.

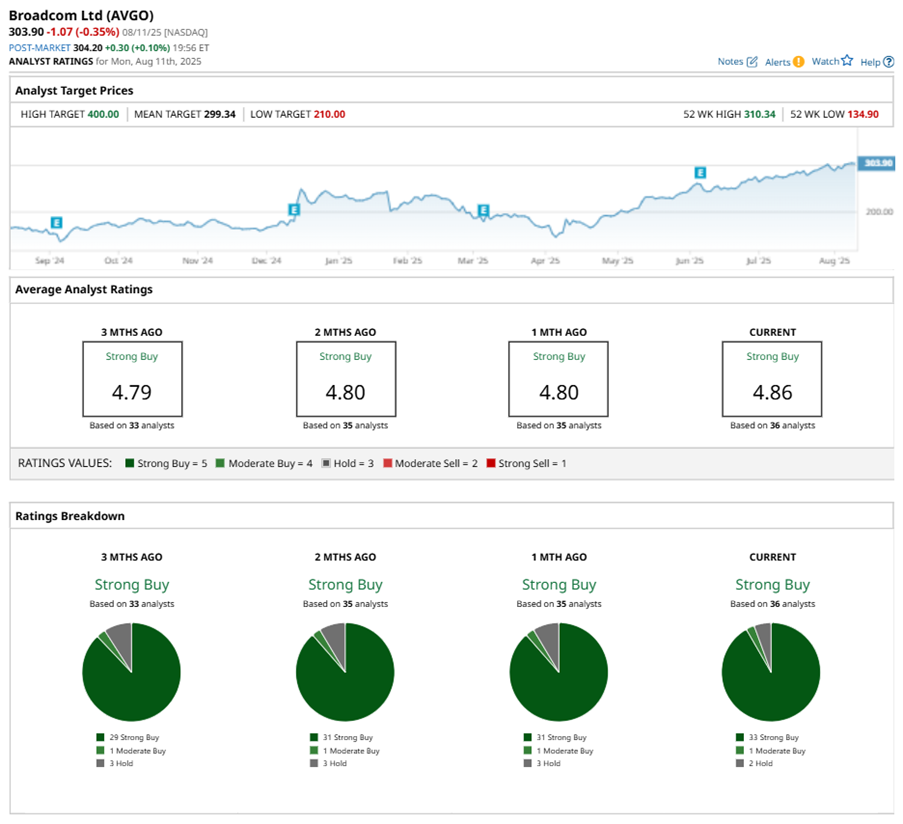

Among the 36 analysts covering AVGO stock, the consensus is a “Strong Buy.” That’s based on 33 “Strong Buy” ratings, one “Moderate Buy,” and two “Holds.”

This configuration is more bullish than a month ago, with 31 analysts suggesting a “Strong Buy.”

On Jul. 30, Morgan Stanley (MS) kept an “Overweight” rating on AVGO and raised the price target to $338, implying a potential upside of 11.2% from current levels.

While AVGO currently trades above its mean price target of $299.34, the Street-high price target of $400 suggests a 31.6% upside potential.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.